Phase one Investment

Phase 1 Investment:

(Retrospective Note: due to the RES equation and American Butterfly part 4, the following has now been enhanced)

Below we see a “starter point” from which to consider the distribution of first phase investment options. A second phase is set after two years later, after which there will be no more options to invest into a US Mother (Anchor) Network.

Investment is split into five groups: Essential Partners, Big Business, Small Business, Governmental Investment and Foreign Businesses.

1. Essential Partners

To create maximum effectiveness for the various S-World software products and initiatives, the products need to be owned collectively by

- The companies that control information technology.

- The technology companies who will assist with the software design.

- Essential patent holders.

- Device manufacturers, in particular television manufactures as Smart TV’s which are expected to gain an ever increasing share of on line sales.

- Creative and administrative Media companies (broadcasters and film makers)

Its early days within this proposal to imagine the scale of S-World commerce; indeed, two more books are yet to be written before any detailed forecasts are offered. However, if one considers everything that could possibly be sold on line over the next century, and halve it, this is the ambition.

The mechanics would work something like this: In Travel for instance, a client purchases a family holiday for $4,000, whereby usually the travel agency would take 20% with their sales agent taking 3%. Instead the sales agent is independent and takes 10% whilst the system (S-World) takes 10% ($400) which it splits between the essential partners.

For instance, if one was on a Dell PC, on a Windows Operating System, using Facebook then Dell, Microsoft, and Facebook may receive $200. Alongside this, the companies that created and continue to create the software and applications receive the other $200.

In basic E-Commerce a 50% mark-up is more common, but the price of goods lowers. This time, if a client is reminded to buy a $150 gift whilst watching “SKY News” on a Sony Smart TV, then Sky and Sony may share $25. Alongside this the companies that created and continue to create the software and applications receive the other $25.

The same applies to search engines, or for that matter any possible way one could buy anything via the internet. The point is that all essential partners see the revenue from S-World as substantial, in many cases more than they would currently receive.

And so adding the “it’s the right thing to do for the planet” and the “it’s the right thing to do for the consumer” (due to the per human results search engine), I hope one can see from the affiliate marketing alone, before we even have a product, it easily has the potential to be the market number 1.

In ten years time, if we consider half of GDP was sold on line, where S-World essential partners had a 50% market share. using today’s GDP of $70 Trillion /4= $17.5 Trillion working on a 25% mark-up, we arrive at a figure of $4.4 Trillion, most of which would be profit generating, at worst creating $3 Trillion in profit.

Essential Partners investment in phase one equals $125 Billion, there is the second US phase and the six global phases tallying up $1 Trillion, returning $3Trillion a year working at our current recession GDP figures, so making the target ROI for Essential Partners 300% per year.

This is before we consider the economic advantages as provided by the network, in particular the Economic Stimulus, the RES equation and the general desire to get the world spending again, as such when one needs to consider not necessarily taking a 50% market share in global E-Commerce, rather a 20% market share of what is already available, but a 30% increase due to new spending and stimulus methods, so the actual potential profitability is far higher.

There are many variations to fully explore. Looking at more specific plans the Facebook example within the following chapter offers a more detailed individual journey, for further analysis and consideration.

It is often best to consider the Network as not necessarily taking market share of GDP, rather taking a little and increasing it as a whole.

If you can’t beat em, join em!

Does the world need another 8,192 TV and device manufacturers? Probably not, But with over 850,000 people per 4 network catchment zone, many receiving network credits, allowing one device manufacturer per 4 networks to set up shop, is not overly saturating. The essential partners will be given such options, allowed to cherry pick any S-World researched technology, be it digital or manufacturing. With such competition, advancement will accelerate creating many new niche brands, some great ideas and new products. All Mother Networks will have the option/licence to become a device manufacturer. Adding new competitors to the market can only increase market share.

Medical Companies: The pharmaceutical companies have been included, in exchange for relaxing patents on pharmaceuticals to those that can’t afford them. In some, or all cases the companies may completely submerge themselves within the network with share holders receiving network credits instead of cash.

2. Big Businesses

With a maximum of $95 Billion in investment options, for a sector that is sitting on over $2 Trillion in cash, most companies will struggle to gain investment options.

This poses a problem of sorts as one does not desire 95% of big businesses to prefer the network was not in existence. To combat this, the idea that should business use the financial software and follow the rules that allow for the M⇔Bst and the RES⇔ equation to boost the economy and remove chaotic factors, general integration into the network as suppliers will take place over time.

3. Small Businesses

Small businesses have twice the investment options that big businesses have, given the software and advantages as presented in their “Suppliers Butterfly” the many small business, with owners not managers running the day to day goings on, will be far more reliable and enthusiastic than their compartmentalized big business counterparts.

It is far easier to get a small business to create a high profit vs. revenue efficiency than it is for a large business.

In general after the Mother Network is created, when it comes to creating its babies, the 50% of investment that will be required, will come from small businesses within the local catchment area of the new Resort Network.

4. Governmental

The governmental allocation was considered, initially simply as a measure for the US government to raise extra funds. However two initiatives have since been considered.

Firstly, in the case of “Spartan Contracts,” which require a property built at cost to be part of the package, getting the “have not’s” on the property ladder, which will have a big social impact. The government could use their allocation to further accelerate this process.

Secondly, in the case of infrastructure, the one aspect lacking from the long term American Butterfly plan, is infrastructure between the new resort networks, railways and highways. Using some of the extra tax income that will become available from the networks to build this infrastructure, assists the network, creates more jobs, increased GDP and in general modernizes America. So it is considered that the USA Government could use there share options to create infrastructure companies within the network, then give their own companies the tenders.

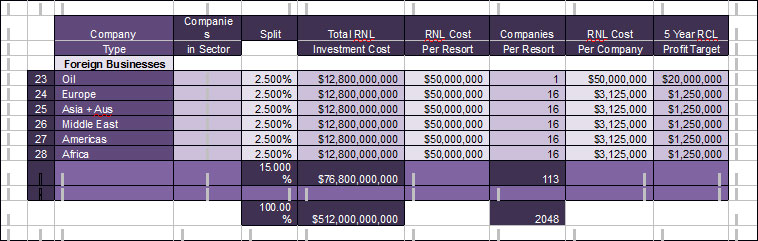

5. International Businesses

15% of options are designated for foreign business.